UK AI operations in 2026 are no longer about hype. This analysis explains how UK companies are actually deploying AI in real operational environments, using proven use cases rather than experiments. In practice, UK AI operations in 2026 are defined by narrow deployment, measurable ROI, and operational control rather than experimentation.

Executive Summary

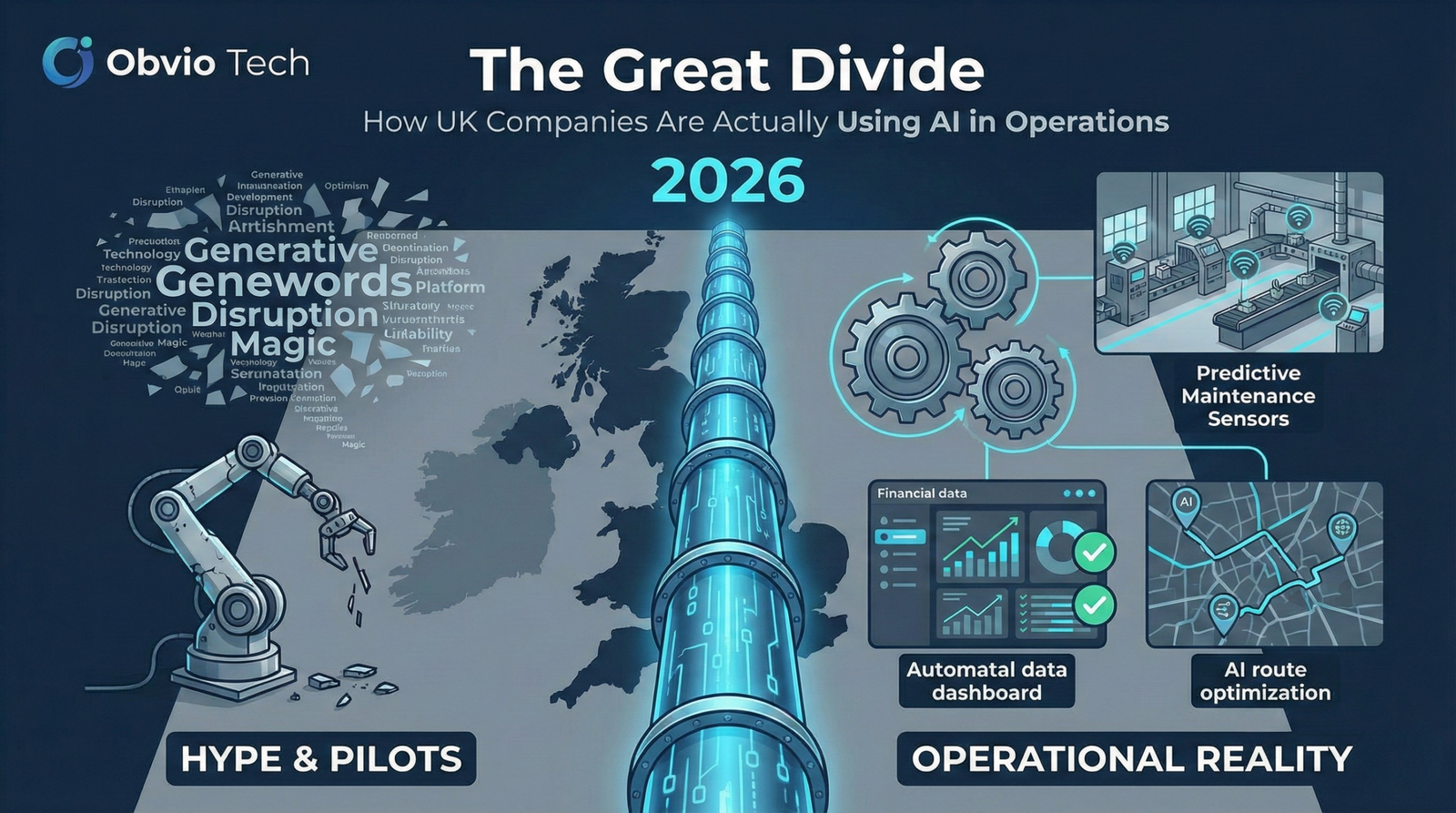

As we enter 2026, the UK technology landscape has fractured into a two-tier economy. While the headlines of 2024 and 2025 were dominated by generative AI’s “creative” potential, the operational reality on the ground is starkly different. We are seeing a widening productivity gap between the “AI-integrated” (predominantly Financial Services, IT, and specialised Manufacturing) and the “AI-hesitant” (retail, construction, and the long tail of SMEs).

For decision-makers, the era of “AI tourism”—running isolated pilots to see what sticks—is over. The market has shifted toward narrow, high-utility operational integration. This briefing cuts through the vendor noise to analyse where UK capital is actually flowing, why 42% of domestic AI initiatives in 2025 failed to scale, and the true cost of moving from pilot to production. This shift clearly defines how UK AI operations are moving from pilots to production in 2026.

1. Beyond the Hype: Where AI Actually Works in UK Ops

Contrary to the “AI does everything” narrative, successful UK deployments are narrow, boring, and highly effective. They focus on friction reduction rather than total transformation.

Financial Services: The Quiet Industrialisation of Compliance

While consumer chatbots get the press, the real value in the City and Canary Wharf has been the automation of RegTech.

Operational Reality:

UK fintechs and Tier-1 banks are using machine learning not to trade, but to clean. Regulatory reporting and Anti-Money Laundering (AML) workflows, previously reliant on large teams manually cross-referencing spreadsheets, are now semi-autonomous.

The Metric:

A 30–40% reduction in false positives in fraud detection among mid-sized UK lenders. This is not about headcount reduction, but reallocating high-cost compliance officers to complex edge cases rather than routine monitoring.

Manufacturing: Predictive Maintenance Over Generative Design

UK manufacturing, particularly in the Midlands and the North, faces a chronic skills shortage. AI is plugging this gap not by designing new products, but by keeping existing machinery operational.

Operational Reality:

IoT-driven predictive maintenance has moved from experimental to standard. Firms are overlaying vibration and acoustic sensors onto legacy assembly lines to predict failures weeks in advance.

The Difference:

Unlike US greenfield “dark factory” projects, UK manufacturers are retrofitting AI into brownfield sites. The ROI is immediate: preventing unplanned downtime, which typically costs £30k–£50k per hour for mid-market operators.

Logistics & Supply Chain: The Brexit / Customs Adjustment

Post-Brexit friction remains a structural reality for UK exporters. AI is being deployed primarily as a paperwork accelerator.

Operational Reality:

Automated customs declaration processing using NLP to classify goods and predict tariff codes.

The Win:

Logistics firms using intelligent document processing report reducing manual data-entry time by up to 70%, offsetting the increased administrative burden of the past five years.

2. The “Pilot Purgatory” Problem: Why 42% of UK Projects Fail

Data from late-2025 shows nearly half of UK AI initiatives never reach production. The failure mode is rarely technological; it is organisational.

The “Shiny Object” Syndrome

Many UK SMEs chased generative AI for marketing and content creation—low-value, high-risk use cases—rather than addressing operational bottlenecks. Projects launched without a hard ROI metric (for example, reducing invoice processing time by 20%) had survival rates below 15%.

The Data Readiness Gap

AI-ready data is not the same as audit-ready data.

The Reality:

A mid-market UK insurer may hold 20 years of records, but if that data lives in scanned PDFs, siloed SQL databases, or unstructured notes, it is operationally unusable.

The Friction:

Around 80% of AI budgets are being consumed by data engineering and cleaning, leaving just 20% for modelling. Executives expecting plug-and-play solutions often withdraw funding once the scale of infrastructure work becomes clear.

3. The Price of Intelligence: The Real Cost of Implementation (2026)

Subscription fees tell only part of the story. The total cost of ownership for a production-grade operational AI system is significant.

Indicative UK mid-market costs:

- Discovery & Audit: £10k–£30k

Assessing whether data is usable. Most projects should stop here but rarely do. - Proof of Concept: £25k–£80k

Prototype development. Often incorrectly treated as sunk cost. - Productionisation: £80k–£300k+

Integration, security hardening, GDPR compliance, and latency optimisation. - Maintenance (Annual): 15–20% of CapEx

Model drift, retraining, and API cost volatility.

The Hidden Tax:

Integration. Connecting modern AI systems to legacy ERPs (such as older SAP or Sage deployments common in the UK) frequently costs more than the AI software itself.

4. Organisational Friction and the “Human-in-the-Loop”

By 2026, “AI replaces humans” has largely been replaced by “AI manages the queue.”

Customer Service:

Pure chatbot models failed in complex UK service sectors. The winning approach is triage—AI handles identity checks and intent classification, then routes cases to humans with pre-filled drafts.

The Cultural Barrier:

Without clear governance, staff often perceive AI tools as surveillance or redundancy threats. This leads to shadow workflows where employees bypass systems entirely, undermining data quality and trust.

5. What This Means for UK Decision-Makers in 2026

For leadership teams, strengthening UK AI operations has become a strategic requirement rather than an innovation exercise.

UK founders, operators, and investors should shift from exploration to consolidation.

UK AI initiatives in 2025. https://www.gov.uk/government/publications/ai-regulation-a-pro-innovation-approach

This analysis fits within our broader coverage of UK-focused AI and automation trends.

## UK AI operations in real business environments.

Final Verdict:

For UK decision-makers, UK AI operations are now an efficiency game, not a demo race.. The hype cycle is dead. Long live the efficiency cycle. The winners of 2026 will not be those with the flashiest AI demos, but those with the cleanest data pipelines and the most boring, reliable operational use cases. Ultimately, scalable UK AI operations in 2026 will be defined by governance, clean data, and repeatable operational value.