Signal Summary

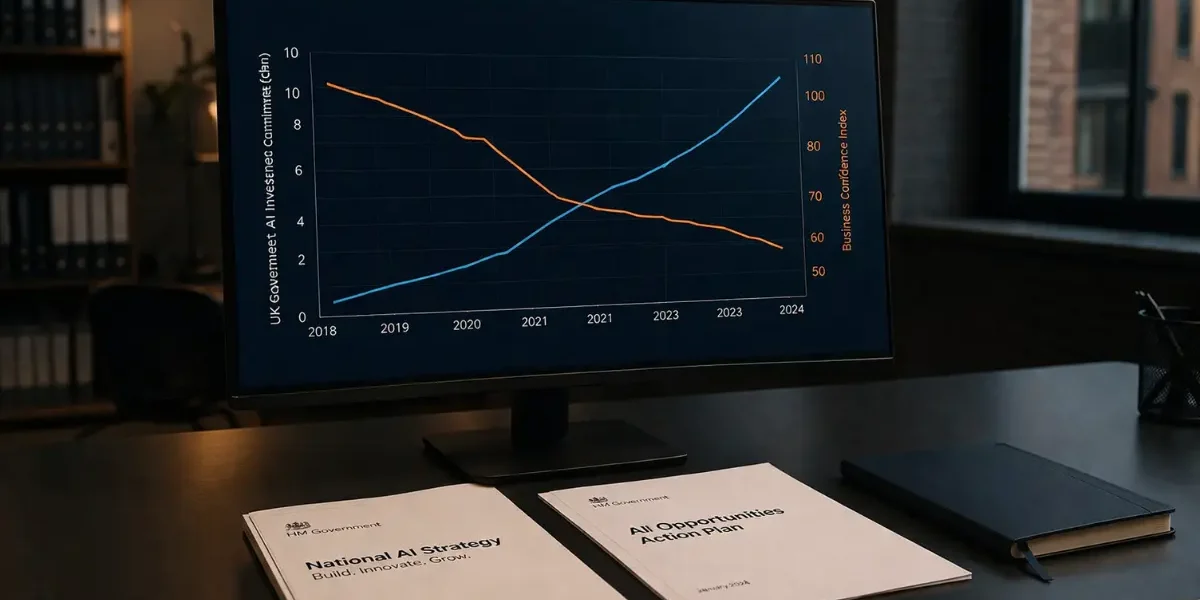

The UK AI strategy execution gap is now measurable. The UK government has committed over £100 billion in private AI investment, scaled compute capacity tenfold, and published a delivery plan with trackable milestones. A techUK survey of 531 business leaders (February–March 2026) found 45% of UK technology businesses have considered relocating — and 83% are actively exploring international expansion. Ambition and confidence have stopped travelling in the same direction.

In January 2026, DSIT’s AI Opportunities Action Plan one-year-on report (GOV.UK) recorded substantive delivery: AI compute capacity grew from 2 ExaFLOPs in 2024 to 21 ExaFLOPs in 2025. UKRI committed a record £1.6 billion to AI between 2026 and 2030. One million AI training courses were delivered ahead of schedule. In March 2026, DSIT announced a £40 million Fundamental AI Research Lab targeting AI’s unresolved limitations — hallucinations, unreliable reasoning, unpredictable outputs. Set against all of that: a simultaneous survey finding 45% of tech business leaders have run the relocation numbers, 38% of non-tech businesses have done the same, and only 37% of tech firms cite growth as their primary 2026 ambition.

Table of Contents

The UK AI Strategy Execution Gap — Why the Divergence Is Structural

The UK AI strategy execution gap is not a communication failure. The government’s delivery record is documented and publicly tracked. The divergence is structural: delivery is concentrated in infrastructure, research institutions, and government-internal programmes — not in the operating environment that private sector businesses experience daily.

The AI Action Plan delivery dashboard (delivery.ai.gov.uk) logs 200,000 people studying AI-related higher education programmes, the Isambard-AI supercomputer operational at Bristol, and the DAWN supercomputer at Cambridge being expanded sixfold by Spring 2026. These are real. But a business owner calculating whether to scale AI operations in the UK is not weighing compute availability at Bristol. They are weighing electricity costs, regulatory clarity, procurement complexity, and whether government speed-to-delivery on promised frameworks matches its speed-to-announcement.

The techUK data exposes the gap at both ends. Among tech companies, 72% still believe the UK can outperform European and North American competitors — but 45% have nonetheless run the relocation numbers. That combination is not pessimism. It is contingency planning.

What Drove the Breakdown

Three structural forces are operating simultaneously, and they compound each other.

Cost pressure. UK data centre operators face the highest commercial electricity costs in Europe (CBRE UK Data Centres Outlook 2026). Grid connection queues now exceed 12 months. For AI-intensive businesses, the cost of infrastructure is a strategic constraint before a single line of model training is written.

Regulatory gap without a framework. The UK has deliberately declined to produce a statutory AI Act, applying existing sectoral regulation instead. For businesses operating across UK GDPR and EU AI Act obligations simultaneously — which is most UK enterprises with any European customer base — navigating two divergent compliance regimes is already a structural cost. Neither jurisdiction offers simplicity. The UK adds the additional burden of running both frameworks in parallel.

Policy delivery lag. The AI Opportunities Action Plan committed to a clear AI Commercial Strategy from January 2026. The DSIT Sovereign AI Unit carries a £500 million mandate. AI Growth Zones have been announced across South Wales, North Wales, Oxfordshire, and the North East. What business leaders surveyed in March 2026 have not yet received is the moment when those commitments translate into a concrete operating advantage — lower costs, faster procurement, or material regulatory certainty — that closes the gap with competing jurisdictions.

Why the UK’s Regulatory Posture Is Widening the Gap

The UK’s light-touch AI regulatory positioning was designed to give it a competitive edge over the EU’s more prescriptive AI Act. In practice, the opposite dynamic is emerging for enterprise buyers. The absence of a clear UK AI governance framework means businesses deploying AI at scale have no domestic regulatory anchor against which to stress-test their systems. The regulatory gap already reshaping enterprise AI decisions is not narrowing — it is producing dual-track compliance programmes that cost time and money neither startups nor mid-market firms have in surplus.

The Cyber Security and Resilience Bill, progressing through Parliament with Royal Assent expected in late 2026, adds supply chain compliance obligations affecting every enterprise using a managed IT provider. That is not a reason to relocate. It is another structural cost that regulators have not yet quantified for the businesses it will affect.

Capital Is Reading the Signals Differently

Investor behaviour has tracked ahead of the survey data. How UK tech policy is re-pricing investment risk has been a documented dynamic since the National Security and Investment Act reshaped deep tech deal structures in 2023. In 2026, that risk calculation has extended into AI venture. Not because UK AI policy is hostile — it is not — but because the cost-adjusted, certainty-adjusted return on UK AI investment is now actively compared against jurisdictions where regulation is settled, compute costs are subsidised, and government procurement frameworks are operational rather than forthcoming.

The DSIT Sovereign AI Unit is explicitly designed to correct this. Speed of deployment will determine its effectiveness. Capital allocation decisions for 2026 are being made now.

What the Execution Gap Looks Like on the Ground

Enterprise behaviour provides the clearest evidence. Enterprise AI procurement consolidation already underway is a direct consequence of the UK AI strategy execution gap at operational level: businesses contracting their AI tool spend in response to cost and compliance pressure rather than expanding capability. Vendor consolidation driven by constraint is structurally different from consolidation driven by maturity. The former indicates enterprises are not yet confident enough in the UK AI operating environment to invest at scale. The latter would indicate the market is rationalising efficiently. The current data supports the former reading.

What to Watch Next

Three indicators will determine whether the UK AI strategy execution gap narrows or deepens through the rest of 2026.

The Digital and Technologies Sector Plan under the Modern Industrial Strategy is the primary one. If it contains specific AI procurement incentive structures and cost intervention mechanisms that directly address the operating environment barriers business leaders have cited, the gap will begin to close.

G-Cloud 15 award outcomes, expected September 2026, will signal whether the government’s £14 billion sovereign cloud framework translates into visible market commitments. Speed of award and SME inclusion rates will both function as delivery proxies.

AI Growth Zone deployment timelines are the third measure. The South Wales zone targets £10 billion in investment and 5,000 jobs. Business leaders will use the interval between announcement and shovel-ready site as a direct read on overall government delivery capacity.

ObvioTech Assessment

The UK AI strategy execution gap is a delivery gap, not a strategy gap. The government’s commitment to AI — in compute, in research funding, in regulatory positioning — is substantive and documented. What the techUK March 2026 data reveals is that the private sector has not yet received that signal with enough clarity or specificity to override the cost and regulatory friction it encounters daily.

The 45% relocation consideration figure is not evidence of imminent departure. It is evidence of businesses that have opened the spreadsheet. Businesses that open the spreadsheet tend to close it with a decision. At the current pace of delivery, more will open it.

The window to convert policy into tangible operating advantage for UK-based AI businesses is 2026. The frameworks are in place. The question is whether they move from announced to operational at a speed that business leaders can factor into decisions they are making today — not decisions they will revisit next year.

Sources

- techUK / Public First: State of UK Tech in 2026 — techuk.org (March 2026)

- GOV.UK: AI Opportunities Action Plan — One Year On — gov.uk (January 2026)

- GOV.UK: AI Opportunities Action Plan Delivery Dashboard — delivery.ai.gov.uk (2026)

- GOV.UK / UKRI: Bold Bet on AI to Keep UK at Forefront of Science and Research Breakthroughs — gov.uk (February 2026)

- Capacity: UK Launches £40m Moonshot AI Lab to Challenge the US and China — capacityglobal.com (March 2026)

- CBRE UK: UK Data Centres Outlook 2026 — cbre.co.uk

For the enterprise-level response to these structural pressures, our analysis of enterprise AI procurement consolidation already underway covers how UK buying behaviour is already shifting in response.